The primary difference is that FHA loans charge both in advance and regular monthly home mortgage insurance coverage premiums, typically for the life of the loan. Nevertheless, they likewise come with low deposit and credit rating requirements, making them one of the much easier mortgage to get approved for. Oh, and FHA interest rates are some of the most affordable around!Let's explore some of the finer details to offer you a better understanding of these common loans to see if one is best for you.

Wondering just how much do you require down for an FHA loan? Your down payment can be as low as 3. 5% of the purchase rate, presuming you have at least a 580 credit rating. And closing expenses can be bundled with the loan. To put it simply, you don't need much cash to close.

However, you can not use a credit card or unsecured loan to money the deposit or closing expenses. Technically no, you still need to offer 3. 5% down. However if the 3. 5% is gifted by an acceptable donor, it's effectively absolutely no down for the customer. For a rate and term refinance, you can get a loan-to-value (LTV) as high as 97.

And remember that the FHA doesn't really provide money to debtors, nor does the agency set the rate of interest on FHA loans, it merely insures the loans. The max loan amount (national loan limitation ceiling) for FHA loans for one-unit residential or commercial properties is $765,600 with the exception of some Hawaiian counties that go as high as $1,148,400 - find out how many mortgages are on a property.

However, some counties, even large cities, have loan limits at the national flooring, which is $331,760. For example, Phoenix, AZ just permits FHA loans up to $331,760. There are other counties that have a max loan amount in between the flooring and ceiling, such as San Diego, CA, where the max is set at $701,500.

Little Known Questions About Hedge Funds Who Buy Residential Mortgages.

Simply put, you truly got ta inspect your county before assuming your loan amount will deal with the FHA.In 2020, limit loan amount will increase from $726,525 from $765,600, while the floor https://www.wdfxfox34.com/story/43143561/wesley-financial-group-responds-to-legitimacy-accusations will rise from $314,827 from $331,760. Loan quantities above the ceiling would be think about jumbo loans, and therefore are not qualified for FHA financing.

This indicates both low-income and wealthy home purchasers can benefit from the program if they so select. Nevertheless, there are DTI limitations that the candidate should abide by, like any other home loan, though the FHA is fairly liberal in this department. It needs to be noted that some state real estate finance firms do have earnings limitations for their own FHA-based loan programs.

The program can be utilized by both first-time house purchasers and repeat purchasers, however it's definitely website more popular with the previous due to the fact that it's tailored towards people with restricted down payment funds. For example, move-up purchasers most likely won't use an FHA loan due to the fact that the profits from their existing home sale can be utilized as a deposit on their new home.

No, reserves are not needed on FHA loans if it's a 1-2 system home. For 3-4 system homes, you'll require three months of PITI payments. And the reserves can not be gifted nor can they be proceeds from the transaction. If you're questioning how to get an FHA loan, practically any bank or lending institution that provides home mortgages will also stem FHA loans, however due to the fact that of some recent infractions not all lending institutions take part in the program.

The best FHA loan provider is the one who can effectively close your loan and do so without charging you a great deal of money, or timeshare vacation deals providing you a higher-than-market rate. There is nobody loan provider that is much better than the rest all of the time. Results will differ based upon your loan scenario and who you take place to deal with.

More About How To Switch Mortgages While Being

Among the biggest draws of FHA loans is the low mortgage rates. They occur to be some of the most competitive around, though you do have to consider the fact that you'll need to pay home loan insurance coverage. That will clearly increase your total real estate payment. In general, you might find that a 30-year set FHA home loan rate is priced about 0.

50% below a similar adhering loan (those backed by Fannie Mae and Freddie Mac). So if the non-FHA loan mortgage rate is 3. 75%, the FHA home mortgage rate could be as low as 3. 25%. Naturally, it depends upon the lending institution. The difference might be as little as an.

25% also. This rates of interest advantage makes FHA loans competitive, even if you have to pay both in advance and monthly mortgage insurance (frequently for the life of the loan!). The low rate likewise makes it simpler to receive an FHA loan, as any decrease in month-to-month payment could be simply enough to get your DTI to where it needs to be.

This explains why lots of people refinance out of the FHA once they have adequate equity to do so. You can get a fixed-rate home loan or an ARMThough most debtors go with a 30-year fixedTypically used as home purchase loansBut their improve refinance program is likewise popularThe FHA has a variety of loan programs geared toward newbie house purchasers, in addition to reverse home mortgages for seniors, and has actually guaranteed more than 34 million mortgages considering that creation.

The max LTV for a cash-out FHA loan is a fairly low 80% (set up in September 2019), below 85% post-crisis (set up in 2009) and an even higher 95% before the home loan crisis occurred. It needs to also be kept in mind that mortgages with less than six months of payment history are not eligible for an FHA squander re-finance.

Some Known Questions About Bonds Payment Orders, Mortgages And Other Debt Instruments Which Market Its.

For those with existing FHA loans wanting to refinance to another FHA loan, the simplify refinance program is a fast and easy option that supplies a lots of flexibility, even for those who lack home equity. Yes, FHA loans can be either variable-rate mortgages or fixed-rate home mortgages. The FHA 30-year repaired loan is definitely the most typical.

If the rates of interest is adjustable, it will be based on the 1-Year Consistent Maturity Treasury Index, which is the most utilized home mortgage index. Absolutely! You can get a range of various fixed-rate FHA products, including a 15-year fixed from many lenders, though the greater monthly payments would most likely act as a barrier to most first-time house buyers.

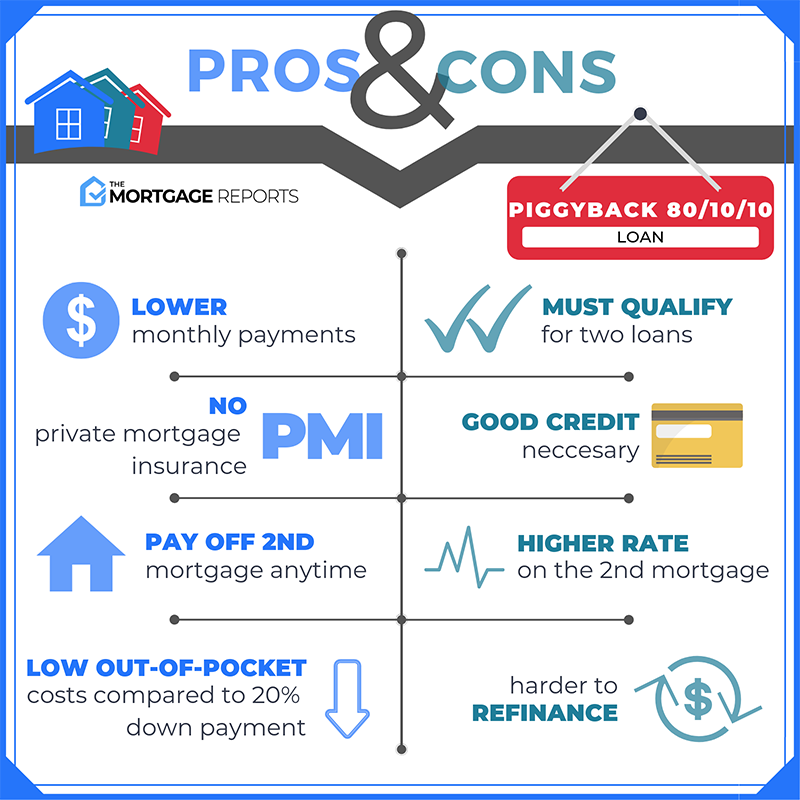

It's possible, though a lot of FHA loans have extremely high LTV ratios, and a lot of home equity loans limit the CLTV (combined LTV) to around 85% -95%, so you'll need some equity before taking out a second home loan such as a HELOC. A second home loan may also enter into play when coming down payment support throughout a home purchase, where the loan is subordinate to the FHA loan.

They have a building program called a $1203k loan that permits FHA debtors to refurbish their houses while likewise funding the purchase at the very same time. Enjoyable fact the standard FHA loan program is technically referred to as the "FHA 203b" in case you're questioning where that name comes from - who provides most mortgages in 42211. FHA loans can be utilized to fund 1-4 unit houses, including condos, made homes and mobile homes (offered it is on a long-term foundation), together with multifamily residential or commercial properties.